In this article, we look through the most demanded header bidding trends over the past year, as well as predictions and forecasts for why they will continue.

1. Video header bidding

Video header bidding has two major advantages for publishers. First, it decreases the latency of video content loading as an auction initiates before the video starts playing. Second, video header bidding brings maximum yield to publishers. The technology allows advertisers to bid simultaneously as opposed to the waterfall model in which DSPs call the bid one by one until one of them offers the price which is higher than the floor rate. Parallel auction in contrast to waterfall brings the highest bid proposed among all participants at once.

It’s predicted that programmatic advertising spending in the United States is projected to reach approximately $290 billion by 2026. And the video formats take more than half of the amount. As for devices, in the Video Advertising market, US$193.4 billion of total ad spending will be generated through mobile in 2028. According to the IAB’s Revenue Report, 2023 programmatic advertising revenue grew to $114.2 billion, with an increase of 4.4% or $4.8 billion compared to 2022. Video ad formats will be in great demand in the following years. So, applying header bidding for video inventory can bring publishers more programmatic yield.

2. Header bidding wrappers

Header bidding wrapper is a technology that was initially developed as a solution on how to organize a large number of buyers. Publishers who work with many advertisers and different header bidding solutions prefer wrappers. The core principle of the header bidding container, as it is also called, is to ensure that all bids are triggered in parallel. It forms the rules for a programmatic auction to bring the highest bid. And in such a way, publishers have more control over their programmatic yield.

Particular SSPs and open-source Prebid frameworks, for instance, develop proprietary wrappers. Many wrappers have been widely adopted by publishers. However, most are based on the flexible Prebid framework, which can be customized to meet publishers’ requirements. Builtwith counts 22,238 websites that are using Prebid globally as of March 2024. Currently, 31% of the top 1 million sites by traffic are using the Prebid wrapper. Only Amazon Transparent Ad Marketplace ranks higher. It is used by 43% of 1 million sites by traffic.

3. Server-side header bidding

Initially, header bidding was carried out on the client side (browser side). A JavaScript code added to a site’s header makes the technology work. It connects all sources of buyers who bid for ad inventory. The downside is that the browser allows connecting to a limited number of sources. Moreover, a large number of advertisers connected to a header bidding wrapper leads to a lower page speed because of running a lot of JavaScript processes on the page.

Speed and page load time continue to be highly important for publishers. And server-side header bidding is much more efficient at this point. The whole process of header bidding auctions is conducted on an external server of the ad tech company. The publisher needs to add a snippet of code on the site, but requests are sent from the ad tech server to all relevant DSPs, not from the browser. Technology is easy to integrate. It allows more demand partners to add to the auction and shrinks page load time.

4. Artificial intelligence and machine learning

Artificial intelligence (AI) and machine learning (ML) technologies have transformed the global economy in recent years, and the advertising industry is at the forefront of this shift. Since 2020, global AI marketing revenue has surged from $12.05 billion to an estimated $47.32 billion in 2025. By 2028, it’s projected to exceed $107.5 billion, driven by a robust compound annual growth rate (CAGR) of 36.6% between 2024 and 2030.

In advertising, AI is transforming how campaigns are designed, delivered, and optimized. By integrating advanced predictive analytics – especially in processes like header bidding – AI analyzes bid data, user engagement, and other key parameters to ensure ads are shown to the right audience with maximum relevance and precision. This results in more efficient ad inventory distribution for publishers and more impactful campaigns for advertisers, redefining the entire digital advertising landscape.

5. Mobile in-app header bidding

Considering the increasing number of mobile apps and in-app mobile ad spending, programmatic buying methods have become a hot topic for the industry. In-app bidding is becoming one of the trendiest technologies for app publishers, though it is at an early stage of development. The AppLovin (former MoPub) advanced bidding tests showed real advantages of in-app bidding, such as an increase of 5% to 15% in publishers’ ARPDAU, an increase in filled supply, an increase in supply access for all programmatic buyers, and an enlarged wallet share for all programmatic partners.

Even though some big tech providers have started to launch in-app solutions, it is still a challenge for most app publishers. The main complication for adopting in-app header bidding has remained a lack of good bits of knowledge on how it works and on the implementation issues, both from publishers’ and advertisers’ sides. So still more lightweight solutions are necessary for the market. Publishers used to appeal to SDK mediation solutions based on the waterfalling method but the quantity of partners is limited and more manual work might be required. The in-app bidding, in contrast to, helps to reduce the necessity of SDK implementation since the solution provides access to a big number of demand partners. Technology is seen as beneficial for publishers, buyers, and mediation platforms alike. But time is needed to make it work for the majority.

6. In-house and customization

IAB Europe reports that 66% of publishers are considering bringing programmatic trading in-house in the next 12 months. The rate has increased from 34% since 2016. This could be explained by the fact that the demand keeps growing, and publishers want to optimize their programmatic ad selling as efficiently as possible and take control of the process. Programmatic in-house brings many benefits, such as ad performance improvement, transparency, and programmatic yield boosting. By implementing an in-house header bidding infrastructure, publishers can make more informed decisions through every step of the process to gain maximum revenue.

Although it can be challenging because of a lack of practical knowledge on operating it, building an internal header beading framework means better monetization for publisher inventory and more operations control. “A third of publishers (35%) are developing in-house operations to gain greater transparency and control of their programmatic processes, ” per the IAB Europe presentation. To start with, by combining in-house operations and external support from ad tech partners, publishers can do their best for themselves.

7. OTT and header bidding

The rise of OTT platforms has changed the way content is consumed and provided new opportunities for programmatic advertising in the area where traditional TV advertising used to be. Viewers are switching to OTT platforms, and the advertisers follow them. With OTT, marketers can target the audience and provide personalized advertising. The implementation of header bidding in OTT gives unique opportunities, and although technically, it is quite a challenge to obtain seamless integration of advertising into content streams with HB in OTT, the vast potential and benefits are pushing development and investment in this area.

8. Privacy and personal data regulation

Introducing new privacy regulations and requirements in the US and EU have profoundly impacted the advertising landscape. These rules have redefined how personal information is handled, pushing the advertising market for better privacy protection and better user control over their data.

With header bidding, publishers offer their inventory to multiple ad exchanges at once, which allows them to earn higher revenue. However, this process often involves collecting and distributing personal user data, such as browsing history, location, and device information. So, it requires new techniques to maintain the effectiveness of monetization strategies without compromising user privacy.

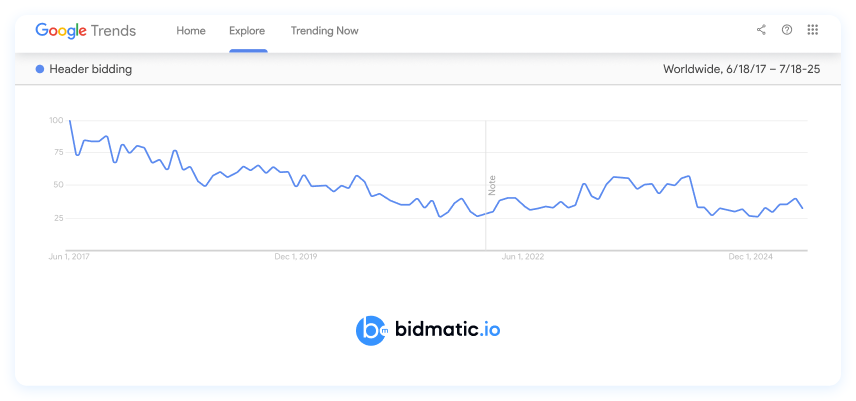

Header bidding in Google Trends: Global interest in header bidding declines, but stability signals maturity

According to Google Trends data from June 2017 to July 2025, global search interest in the term “header bidding” has experienced a notable decline over the past eight years, signaling a shift in how the industry engages with the technology.

In the early years (2017 – 2019), header bidding enjoyed peak popularity, driven by growing publisher adoption and widespread industry excitement. During this period, search volume was consistently high, indicating active exploration and implementation across the digital advertising ecosystem.

However, starting in late 2019, interest began to taper off. By 2020 and 2021, the trend line had settled into a lower, more stable range. From 2022 onwards, the volume of searches remained relatively flat, with only modest fluctuations. This plateau suggests that header bidding has moved from the “exploration” phase into a state of normalization and mainstream adoption.

Interestingly, there was a small rebound in early 2023, potentially tied to developments such as server-side header bidding upgrades, growing publisher interest in privacy-compliant monetization strategies, or regional market shifts. However, this bump was short-lived, followed by another drop in late 2023, and stabilization throughout 2024 into mid-2025.

The regional breakdown adds further context. China leads with the highest relative interest, followed by Israel, South Korea, and Singapore. China’s dominance reflects the rapid digital growth in its publishing and adtech sectors, while Israel’s strong position is consistent with its reputation as a hub for advertising technology innovation.

Ultimately, the declining trend in search activity doesn’t signal obsolescence. On the contrary, it’s a sign that header bidding is no longer novel – it’s embedded in the core infrastructure of modern programmatic advertising. As the market matures, attention is shifting toward complementary innovations like Prebid server optimization, seller-defined audiences, and cookieless targeting strategies, all of which will shape the next era of programmatic monetization.

The most significant header bidding facts of 2022-2025

- As of the first quarter of 2022, header bidding was used by 70% of online publishing websites and by 16% of the top 100,000 websites in the United States to boost eCPMs, increase fill rates, and maximize revenues.

- Although 86% of publishers have been approached by a header bidding provider, only 53% have adopted the technology. The main barriers to adoption include a lack of information (29%), uncertainty about the value it provides (20%), and concerns about the internal development time required (19%).

- Transparency and revenue growth remain crucial for publishers. At this point, header bidding is doing great work for media companies. The 1+1 media’s header bidding integration caused 25% ad sales income growth.

Final Thoughts

Header Bidding changed the programmatic advertising industry, bringing more transparency and forecasting for better business strategy for publishers and their partners. This technology became more affordable as many supply-side platforms provided free access and connection. This method of ad buying infused many benefits into the media supply chain, and it will last and develop in 2025.